NSSF Contribution Rates Set to Rise in February: What You Need to Know

As Kenyans brace for the second year of the implementation of Tier 1 and Tier 2 NSSF contributions. A familiar pang of anxiety sets in with the looming rise in contribution rates. Headlines like “More pain as NSSF Rates set to go up next month” (Daily Nation) capture the sentiment of many, but is this truly the whole story? Let’s delve deeper into the evolving landscape of NSSF contributions.

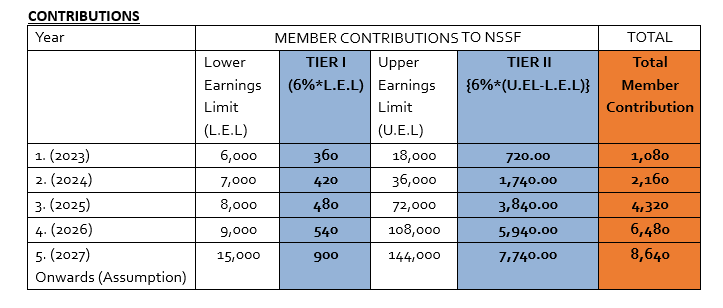

This is what you need to know: the Lower Earnings Limit rises from Kes. 6,000 to Kes. 7,000 with contributions rising from Kes. 360 to Kes. 420 for TIER I Contributions while the Upper Limit doubles from 18,000 to Kes. 36,000 with contributions rising to Kes. 1,740 from Kes. 1,080 which makes TIER II Contributions. Employers will match both these contributions.

Year 2 Contribution Rates 2024

|

Lower Limit (Tier I) |

7,000 |

|

Total Contribution by Employee |

420 |

|

Total Contribution by Employer |

420 |

|

Total Tier I NSSF Contributions |

840 |

|

Upper Limit (Tier II) |

36,000 |

|

Contribution on Upper Limit (6% of Upper Limit less Lower Limit) |

29,000 |

|

Total Contribution by Employee |

1,740 |

|

Total Contribution by Employere

|

1,740 |

|

Total Tier II NSSF Contributions

|

3,480 |

|

Total NSSF Contributions |

4,320 |

How did we get here? Tier I is 6% of the Lower Limit which is 6%×7,000 = 420 while Tier 2 is 6% of the Upper Limit less the Lower Limit which is 6%× (36,000-7,000) = 1,740. The contributions will be graduated for the first four years after the commencement date (February 2023) in accordance with the table below.

NSSF ACT,2013 IMPLEMENTATION TABLE

A quick reminder:

- Tier II contributions may be paid to the Employer’s Occupational Scheme or Umbrella Scheme (E.g Octagon Umbrella Retirement Scheme) upon an employer making a written application to contract out of NSSF and obtaining approval from the Retirement Benefits Authority.

- The written request to the Authority of the intention to opt out shall be made at least sixty (60) days before the desired opting out date. The employer who opts to contract out shall conduct a member sensitization on the implications of the act and sign the relevant documents to be submitted to the Authority for approval.

- Octagon Africa Umbrella Retirement Benefits Scheme has received its Reference Scheme Test and therefore approved to receive NSSF Tier II contributions.

- We will support the Participating Employer apply for opting out NSSF tier II contributions. On receipt of documents, the Authority shall within thirty (30) days from the date of receipt of an application for contracting-out from an employer, determine whether the employer has fulfilled the requirements for contracting-out, and in such case, it shall issue and send to the employer concerned a Contracting-Out Certificate with a copy to the National Social Security Fund.

- An employer who has been issued with a Contracting-out Certificate will make an application in writing to the National Social Security Fund for transfer of Tier II Fund Credits from the National Social Security Fund to the contracted-out scheme and on receipt of the application, the Fund shall transfer the Tier II Fund Credits in respect of each of the employees in the contracted-out scheme.

- On attainment of retirement age, a member will access their NSSF Tier I and Tier II contributions in the manner stipulated in the act as follows; a third (1/3) of the entire fund as a lump sum benefit, and the balance, two-thirds (2/3) the member will choose an insurance provider of their choice to purchase a monthly pension (annuity) or Income drawdown Fund. The Annuity must be a life annuity with at least 10-year guarantee period.

- On access of the funds at retirement, the provident funds will be accessed as per the requirement laid out in the Trust Deed and Rules (Deed of adherence). However, the NSSF Tier II contributions in the scheme will be accessed as per rules laid out in the the NSSF Act No. 45 of 2013 as explained above.

Benefits of Opting out NSSF Tier II contributions;

- Higher Return Potentials in a private pension scheme arrangement following a highly regulated scheme expenses and a prudent investment structure of these funds.

- Efficiency in accessing member statements and claim of benefits online in Octagon Umbrella Retirement Benefits Scheme.

- The Governance Structures for our scheme allow for member engagement sessions and clear reporting structures.

- Managing Cost – The cost of running our pension scheme is low and largely regulated, which improves the return and growth of the pension fund.

- Value Addition – Free trainings for members of our scheme on financial literacy, retirement options, and customized products e.g. Group Life Assurance & WIBA

Your Employees deserve the best! Let us assist you in making the optimal choice for your retirement funds.

Reach out to us at businessdevelopment@octagonafrica.com or call us on 0709 986 000 for a presentation from our team.